Editorial > Blockchain - The Technology that's changing the World Block by Block - Part 2

Blockchain - The Technology that's changing the World

Block by Block - Part 2

Dais Feature | 17/02/2021 05:03 PM

Blockchain is not a household fuzzword and whenever it's mentioned, more difficult names like Cryptocurrency... Bitcoin... Ethereum.. are thrown around. Sometimes understood. Mostly misunderstood. From the last time we touched upon the tip of the colossal iceberg that's Blockchain – much has changed around the world...

From a ‘Dark Web’ concept, Blockchain and crypto is out there legitimizing its presence every growing day. From governments perceiving the technology and its resultant outcomes (read: Bitcoin) as a threat to its traditional methods of working and fiat currencies – there is fast-moving acceptance and even innovation coming through from the powers that be for this blitzing soon-to-become-mainstay of the future. As we speak, the Government of India drafts a proposal to ban cryptocurrencies again and Elon Musk announces to accept Tesla payments in Cryptocurrencies!! Funny world ain't it?

Can we afford to ignore it anymore – that question was well answered the last time when we covered the Basics of Blockchain in our Block by Block Part 1 Feature. But if we were to adapt it, learn it, imbibe it and make it a close part of our ecosystem. . .

What are the implications we are looking at?

What are the advantages of embracing this technology? And of course, what are the threats?

We have renowned Blockchain expert Raj A. Kapoor with us, who piqued our curiosity with his lucid insights on the larger outline of Blockchain in our First Part of Block by Block. He also gave us a primer of what’s coming up in the next part of his feature – what are the uses of Blockchain, where is it being applied, how are the corporate giants embracing it and what is the adoption of this technology looking like, in the future for India.

Let's dive into the second part of Block by Block with an endeavour to seek these answers…

The Instantaneous Blockchain - Blink and You MISS!

Here’s a thing about blockchain—it can be really fast! Blockchains, built for speed can process and verify transactions more quickly than the alternative systems. When we explained the functioning of Blockchain in our First Part through a real-life use case of a laptop purchase chronology, it seemed to be a tedious and labour-intense process. The first thought that comes to mind then is - if everyone has to copy everything that happens to the chain, it is definitely more time, cost and manpower absorbing than normal ‘siloed’ record-keeping. But in fact, these transactions get processed by computers in milliseconds.

The reason why blockchain can be much faster than the alternative is because it’s decentralized (and therefore, "lighter”), so let’s talk about that to achieve the definition.

Bl ockchain Is Decentralized

ockchain Is Decentralized

A lot of Blockchains operate with no central authority. The technology is built in a way that it can let people or companies add and verify their transactions—without a single governing body intervening at any point in the process flow. We explain this with an example:

Amit pays rent to his landlord Baburam. What would be the sequence of events followed here:

1. Amit prepares a cheque - Writes the name of the recipient, the amount of the cheque, the date of the payment and signs the cheque.

2. He gives it to Baburam.

3. Baburam deposits the cheque in his ABCD bank.

4. ABCD bank processes the cheque, taking a few days to verify that all the information is correct, there are sufficient funds in Amit’s account to honour the cheque, and that the cheque isn’t counterfeit.

5. Finally, Baburam receives the rent money.

Meanwhile, if Amit were paying with a blockchain-based currency, the transaction would have been just one step -

- Amit deposits the money to Baburam… and … that’s it.

- None !!

The transaction gets recorded on the blockchain, Baburam’s blockchain verifies the transaction, and everything is set. Decentralized blockchains essentially cut out the middleman.

Here’s what a blockchain looks like with more than just you and your landlord participating:-

When one copy of the blockchain ledger gets changed, they all verify that transaction before adding it to their own ledgers. And blockchain is faster than the alternative, because everybody involved doesn’t have to wait on a single, slow-moving source for verification. It all happens simultaneously.

The Blockchain is Democratic - A New World Order?

So far, we’ve got that a blockchain is a digital ledger shared between a network of people. Each participant can manipulate that ledger, recording new blocks of data onto the chain, but with each transaction, the entire chain gets analyzed by everyone to make sure it’s still accurate. In other words, everyone has their own copy of the ledger, but nobody can make a change without everyone agreeing to it.

It is a democratic system with its Three Main Constituents functioning as its basic framework:-

- A network of computers/participants

- A network Protocol

- A consensus mechanism

Depending on the permissions of the blockchain, it can be public, and open to anyone with a computer, or private, accessible only by specific members. Each computer is called a node, and it makes up one part of the network of participants in the blockchain.

A network protocol is, in simple English, a rulebook that determines how those nodes can talk to each other. Typically, each node has its own copy of the general ledger (the blockchain) so there’s protection against mistakes or fraud.

That redundancy, called “fault tolerance,” is what makes blockchain unique.

Finally, the consensus mechanism is the process by which a blockchain network verifies transactions and comes to an agreement on what the current, accurate blockchain is.

Do you remember the laptop example in the previous part? How people in town knew that Rishi wasn’t allowed to sell laptops and that the amount mentioned was way too expensive for a simple no-frills laptop? Those sorts of rules were agreed upon beforehand by every node in the network—they’re a defining feature of the network. If they didn’t exist, then anyone could sell laptops like those for however much they wanted.

Public blockchain networks tend to have pretty high standards for security, while private networks might be a little more trusting. But either way, the rules that form the consensus mechanism are what gives blockchain technology its flexibility and power. Anyone, individually, can check the validity of each transaction and come to a conclusion on whether it’s good or not.

The 3 PILLARS of the BLOCKCHAIN DEMOCRACY

1. People or companies dealing with each other

2. A relationship between those people or companies

3. A rulebook they all agree on that explains which transactions are okay and which are not.

The Key Advantages of Blockchain

Blockchain technology has 4 big advantages:

Transparency

Since everyone in a blockchain network has access to the ledger and the rulebook, nobody involved gets left behind. You can see who owned or paid or gave or did what, at various points in time, whenever you want or need. It’s a totally transparent system. Furthermore, to ensure there are no nefarious nodes added to the blockchain, blockchain networks require new computers to participate in a “consensus test” (more on this later) to ensure they are trustworthy. If a computer passes the consensus test, they become eligible to add blocks to the blockchain. Something like clearing an entrance exam! This process is what those in the cryptocurrency world call “mining.”

Security

Since everyone has a copy of the ledger that they use to validate the newest version, it’s a democratically secured system, too. There’s no single company or agency with extra power. Everyone is in charge. Furthermore, new blocks on the blockchain are always stored linearly and chronologically. After a block is added to the chain and receives its own hash, it is virtually impossible for a hacker to alter that block without having to then go back and alter every preceding block in the chain (which would require an immense amount of computing power).

Instantaneous Transactions

Blockchain transactions can take way less time than transactions that involve some sort of middleman, simply because they are self-validating.

No Central Authority

This one might sound a bit abstract—who cares if some sort of authority is watching over your transactions?

But here’s the deal: When there’s a middleman, that middleman tends to slow things down and skim off the top, taking transaction fees and charging late penalties and all that business. In Blockchain, there is no central authority.

The Double-Spend Problem is Solved

Because digital money is just a computer file, it’s easy to counterfeit with a simple “copy and paste.”

Without blockchain, banks keep track of everyone’s money in their accounts, so that no one “double-spends”—or spend the same money twice. Blockchain solves this problem differently and more efficiently than banks: it makes all transactions and accounts public so it’s blatantly obvious when money is being counted or used twice.

Gist of the story…

Using blockchain can potentially speed up transactions while cutting costs associated with third-party banks and lowering the risk of fraud. That means more speed, affordability, and security for everyone.

A Few Disadvantages of Blockchain

Surely there are a few challenges towards implementing Blockchain:

For Blockchain to Work, Everyone Needs to Co-operate

In order to belong to a blockchain network, each company needs to be upfront and forthcoming about their own security protocols. Transactions added to the blockchain need to be transparent to everyone else, so they can verify the blockchain—that’s the point.

Which means that, while a blockchain can be encrypted to protect itself against hackers, the data in each block can’t be. Companies might be understandably hesitant about removing some of their safety features in order to accommodate blockchain technologies, and for good reason.

Getting everyone on a blockchain network to “agree” to certain kinds and levels could be difficult—and implementing those additional security layers is another hurdle altogether.

Blockchain Isn’t Regulated Just Yet

The government isn’t quite sure how to handle it—and neither are many companies. It’ll take some time before regulations and laws governing the use of blockchain get written, especially in the financial sector, but they’re bound to come up sooner or later. And that’s an uncertainty that not everyone is comfortable with.

Blockchain Could be Hacked, Raising Security Issues

Blockchain as an idea is pretty secure. Everyone double-checks their records to make sure there’s no fraud going on. But what about hacking? If a bank gets robbed, it just loses its own cash—but if a blockchain gets hacked into and 40 banks are on that network, then a lot more damage could be done.

The potential dangers here haven’t been fleshed out completely, but it’s something to keep an eye on. However, with the ever-involving technology, this issue is being quickly addressed and mitigated.

Complexity

As you can tell by now, a simple explanation of blockchain technology isn’t easy. To really understand blockchain, it pretty much requires adopting an entirely new vocabulary with words like “hash,” “nodes,” and “mining.” Because of this, it has taken quite a while for blockchain to finally get the mainstream appeal.

And … Who Uses Blockchain? Or Who Shall Use Blockchain?

Banks and financial services are already using blockchain to cut out the middlemen—and a lot of time, money, and risk—when dealing with monetary transactions.

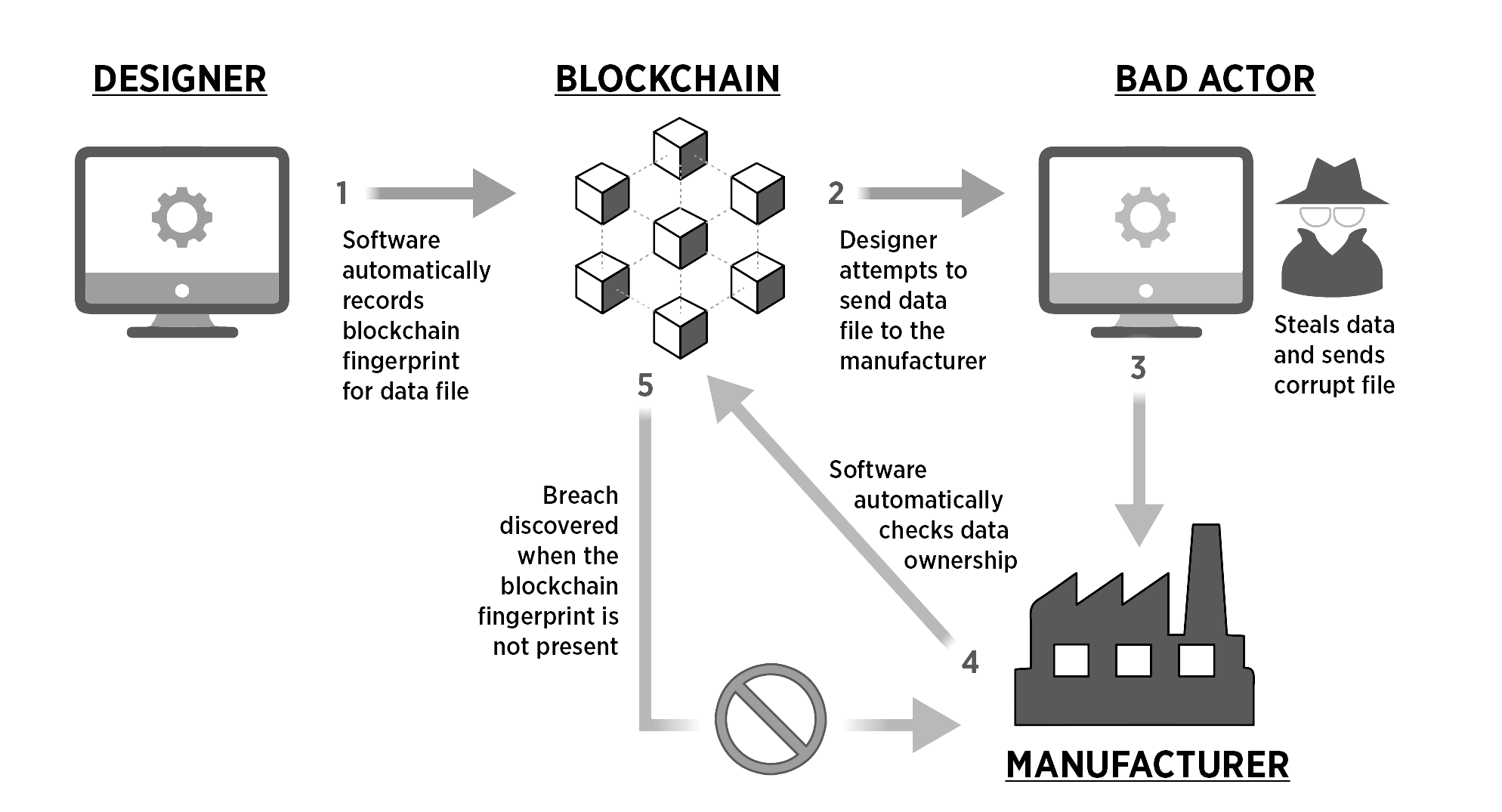

Industries that are at high risk for fraud are starting to use blockchain to verify their wares. Supply Chain Management, Inventory Management are some of the quick adapting industries to blockchain technology. A few companies are implementing blockchain to prevent the false certification or sale of blood diamonds and stolen art, for example.

Digital content like music, movies, and online ads could use blockchain to prevent piracy. By using new file formats that can play the media and encode blockchain data that reflects intellectual property and payment history, musicians and filmmakers wouldn’t be losing out on millions.

In healthcare, blockchain technology can be used to prevent the theft of pills through the supply chain and give medical history ownership back to patients (who can distribute it to their doctors, for certain amounts of time, as they want or need).

In healthcare, blockchain technology can be used to prevent the theft of pills through the supply chain and give medical history ownership back to patients (who can distribute it to their doctors, for certain amounts of time, as they want or need).

In the food and beverage industry, farmers could use blockchain to monitor their crops—and trace where and when food recalls occur. As we say nowadays, from farm to fork!

Insurance could be dramatically changed. Imagine a world where you can get insurance that lasts for a few hours, like when you’re doing some extreme sport. Or where taxi drivers can bypass insurance companies by combining their money together on a blockchain and creating a safety net for themselves.

Blockchain could help in politics by minimizing Election fraud and increasing voter turnout. Each vote could be stored on the blockchain, making it impossible to alter. The blockchain could also increase transparency, while lowering the manpower needed to administer an election.

While it seems like a dream come true for a country of our size and diversity, it also must provide some food for thought to the powers-that-be!

Supply chains can use blockchain to record product status at each stage of production. Because blockchain is permanent and unchangeable, it makes it possible to trace each product to its source.

Manufacturing, even Charities and Crowdfunding are getting on to blockchain.

Blockchain is a development that lends itself to creativity and it is only growing exponentially. But it still has a limited reach – it remains restricted to large organizations – the big corporates and in some ways, the government. Who misses out in this big-boys game then? We, the people.

The small business owners, the retail investor, the common man who has only been exposed to one aspect of the Blockchain Technology – Cryptocurrency or even granularly, Bitcoin. It is to this large majority, that we wanted to explain the Blockchain concept in simple parlance, demystifying the jargon associated with it and prompting ideas to learn more and possibly invoke the adaptation of this ecosystem that now surrounds us, our awareness and acceptability of it, notwithstanding.

The third part of our Feature will bring the discussion down to brass tacks- actual uses and probable applications for us – the future-gazing next generation. Stay tuned, as the chances are many.

R A J A. K A P O O R is an Advisory Board Member at several Blockchain companies and is the Founder and Chairman of the Indian Blockchain Alliance - the largest Indian emerging technology think tank. Raj is an accomplished Tech innovation professional, Drupal Web Application Developer, Blockchain & Cryptocurrency Educator, Certified Bitcoin Professional (CBP), Blockchain Solution Architect, Community organizer and a friend of disruptive ideas, protem Chairman for Organization of Blockchain Technology Users (OBTU).

R A J A. K A P O O R is an Advisory Board Member at several Blockchain companies and is the Founder and Chairman of the Indian Blockchain Alliance - the largest Indian emerging technology think tank. Raj is an accomplished Tech innovation professional, Drupal Web Application Developer, Blockchain & Cryptocurrency Educator, Certified Bitcoin Professional (CBP), Blockchain Solution Architect, Community organizer and a friend of disruptive ideas, protem Chairman for Organization of Blockchain Technology Users (OBTU).

His thoughts can further be accessed Here.

You were reading a Dais Editorial©2020

If you loved reading this Feature, comment on our social media handles and spread the word.